The Dawn of Chaos

Put Joe Rogan in charge of the Fed!

The Painful World of Reality

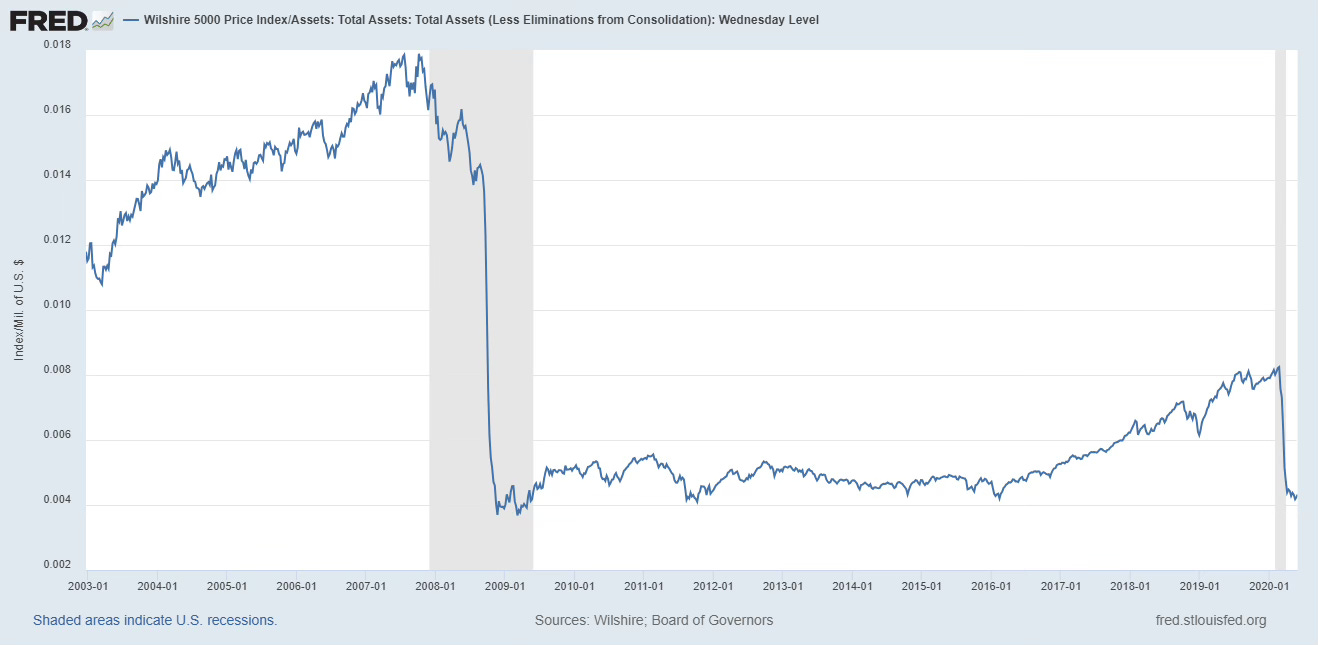

I don’t like this chart. Stock prices have failed to keep up with the expansion in the Fed’s reserves. I have so many problems with this. Sorry guys, life’s way more complicated than that... but it did get me thinking. I’m a sucker for such things: for seeing the flaws in everything.

Remember the film, The Matrix? Morpheus offered Neo the choice of two pills – blue, to forget about the Matrix and continue to prosper in a world of illusion, or red, to live in the painful world of reality. Guess which one I’m choking on?

But first that chart. We need the bigger picture. So let’s take 1980 as the starting point to capture the broad cyclical sweep of modern time that began with man’s ambition to quantitatively reduce the amount of money in circulation and ended instead with his intent to expand the very same money balances... does no one else see the irony!?

Then broaden the composition of the index to the Russell 3000 – more is better – and then adjust for inflation... because the dudes with pitchforks don’t give a DAMN about the Fed’s chicanery. They care only that the stock-market is keeping pace with the inflation experienced by real ordinary households.

Conveniently, the period divides evenly into two. The first is the Michael Jordan era of economic perfection: less government, less monetary inflation and more powerful economic expansions. What followed was lots of hot air – more and more monetary injections and the ensuing chaos we are experiencing NOW.

Returns were really good – and then a bit blah

The inflation-adjusted returns from the Dow Jones Industrial Average over that first 20-year period, with dividends reinvested, was an astounding 12.5% p.a. – you were almost doubling your money every five years. You can handicap a bull market like that with inflation or the expansion in Fed money or indeed anything else you care to mention – it doesn’t matter, as stock prices climbed FOR REAL!

Equities have continued of course to make new real all-time highs, albeit at a slower pace: that real return has been dialled back to 4% these days, which isn’t a disaster. A high is a high! And we’ve hit real as well as nominal highs so – end of story? Stop here and live happily ever-after? Or not? It’s for you to decide...

The Great Paradox

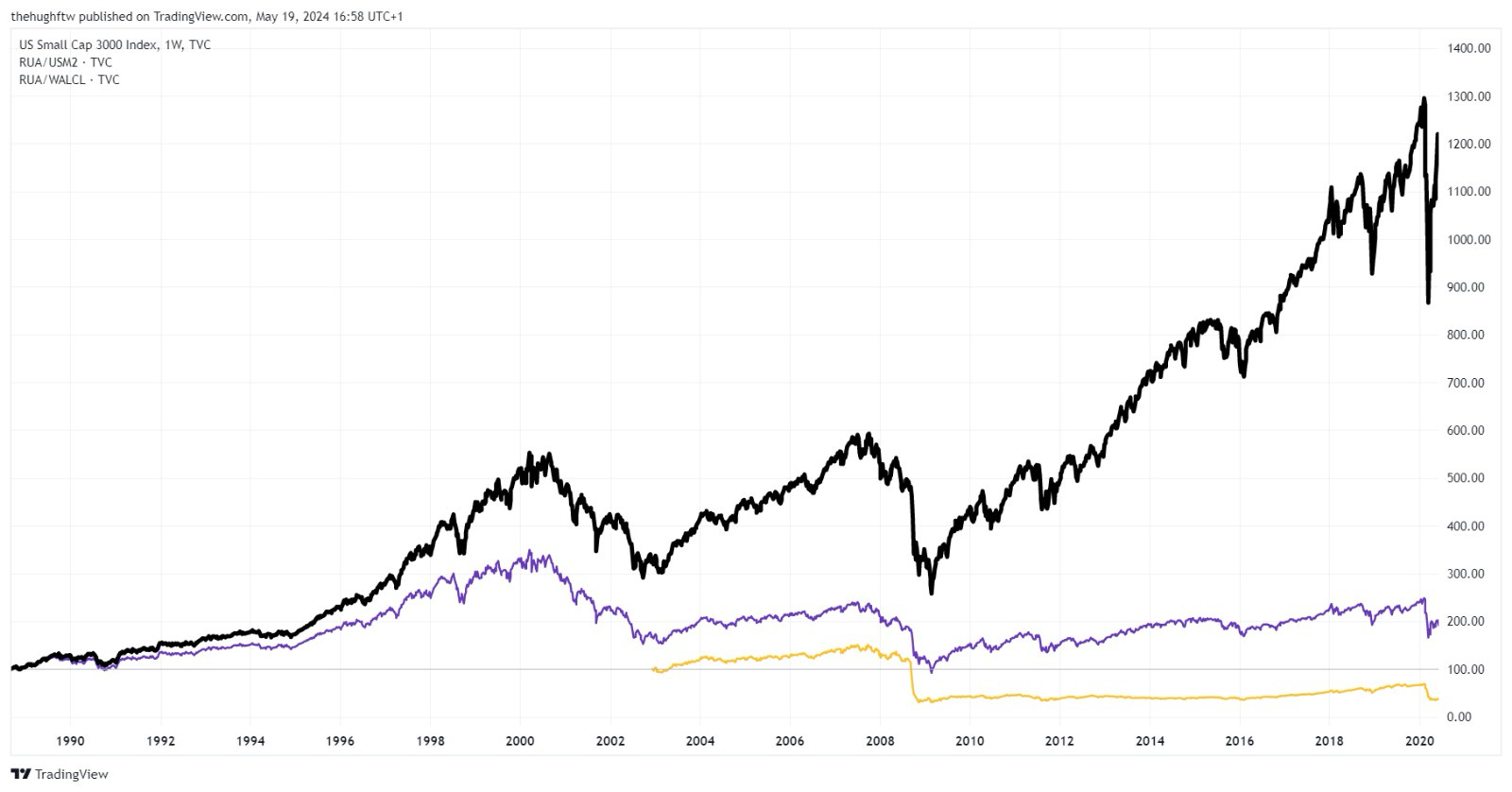

My problem with the original chart is that it doesn’t speak to the great unspoken paradox of the global central-banking community’s monetary activism since the year 2000 – that is, the stark contrast between the explosive growth of inert central banking reserves and the less expansive, but more economically potent, growth in commercial bank assets. And that’s where things get interesting.

Denominated by the Fed’s monetary expansion, the gains since the year 2000 turn into losses... preposterously high losses: we’re trading 85% below the late 1999s high. I’m pretty sure this is irrelevant... We’ll see later on.

But when those gains are handicapped by just the growth in private-sector US bank assets, the drawdown is a lessoutlandish c.30%. Now that is certainly worth exploring further.

First a clarification: I am not shouting HOAX! and claiming the Fed has invented the entire bull market. But it has always been my belief that to catch a glimpse of the future you need to be acutely aware of relative price charts; that positions go right, or wrong, FIRST, relative to a basket of other risk assets. So, what’s going on with the relative relationship between stocks and money? And why haven’t stock prices, if anything, gone even higher?

It isn’t duplicity. Bank credit growth drives GDP growth. Infuse banks with either the confidence to lend, or provideregulatory diktat and a guidance window as per “The Princes of the Yen”, and watch with wonder: asset prices always climb both nominally and when deflated by the growth in loans as demonstrated by the chart of the Japanese stock-market deflated by the immense growth in broad money during the 1980s. Loans expanded at 15% p.a, between 1986 and 1989, but stock prices soared more.

That asset prices have been unable to keep up with broad money supply growth ever since, both in Japan and elsewhere, is truly concerning. What’s changed?

I want to take you back to the launch of my hedge fund way back in the final quarter of 2002 to attempt an answer.Because it was only one month after my launch that Fed chief Ben Bernanke gave his famous helicopter-money speech, which gave notice of the explicit money-printing programs of the Federal Reserve to come, and only 18 months after the Bank of Japan had actually implemented the first modern such scheme.

The Theory of Central Banking

No active investor today lived through the great inflations of Germany in the early 1920s, nor the outbreaks that scared several European countries as well as China and Japan in the 1930s and into the 1940s. And so, it might be argued that our modern economic thinkers are in a situation similar to Plato’s chained cavemen seeing shadows of (monetary) reality projected on the wall (screens) in front of them.

To these wise heads, pure logic, unfettered by the noise of empiricism, leads them to conclude that as fiat money, unlike other forms of government debt, pays zero interest and has infinite maturity, then central bankers can issue as much of it as they like, allowing them to acquire indefinite quantities of goods and assets.

This is impossible in equilibrium, they reason – i.e. something’s got to give – and so they conclude that fiat issuance will always and everywhere raise the price level even if nominal interest rates are at the lower bound. Owing to the absence of empirical observation, pure reasoning like this is, as Plato argued, perfect.

This is a Minority Report that always concludes with inflation being always and everywhere a monetary phenomenon.

The Birth of Tragedy

One of the philosophers, by happenstance unchained, leaves the cave and is free to stroll with the happy people bathing in the sunshine. He is shocked to discover that, almost 20 years after the Bank of Japan initiated central-bank money printing, the world is not experiencing inflation as his cave- dwelling colleagues had predicted. Instead, the world’s credit markets are steadfast in their belief that deflation is the more likely outcome. For Christ’s Sake! The 10 Year US Treasury yield touched 0.5% just last month!

He rushes back to the cave to inform his fellow elites of his discovery – that inflation is not a monetary phenomenon after all – but is dumbfounded by their intolerance of this insight. He discovers that perhaps great men may indeed make great mistakes... that their perfect conception of a perfect global monetary system is fallible...

And if today’s central bankers have seen the outline of the perfect monetary system, are they not then intent on debasing our monetary system? How else can you rationalise the experience of Japan, where the central bankrecently launched its 27th iteration of QE? Why don’t they get it?

And what of gold, the soul of this soulless system? Can it be the financial equivalent of Disneyland?

Disney puts people in a costume and we make believe they are the living embodiment of Mickey Mouse on Earth. The simulacrum of gold is governed far from holiday parks in Florida, of course, by the scriptures of our governing monetary elite in Washington, Frankfurt and Tokyo.

Few are the brave men willing to question great men. Believe me, I have tried; I really tried. But in the end, this truth, that printing reserves is inevitably inflationary, seems irrefutable.

A Hero’s Journey

This really depresses me because I’m forced to ask myself, was it really my exercise of free will that had me buying gold in 2003 just after Bernanke’s original speech? Was it really a surprise that the price tripled in the great commodity boom prior to the demise of housing and the US financial sector in 2008 as others reflexively joined me and reinforced a trend searching for a reality?